A realistic budgeting setup with a credit card statement, notebook, and score-style phone screen. The phone interface is illustrative, not a real app screenshot.

A good credit score can help you get approved for a flat, phone contract, car finance, mortgage, or lower-rate loan. However, many beginners think building credit means taking on debt they do not need.

The good news is simple: you can build credit without getting into debt. The safest approach is to use credit lightly, pay on time, keep balances low, and check your report regularly.

This guide gives you 10 practical ways to improve your credit score while protecting your financial health. You will also see realistic examples, tool suggestions by region, and simple routines you can repeat every month.

What Is Credit and Why Does It Matter?

Credit is your ability to borrow money and repay it as agreed. Your credit report shows your history with accounts, payments, applications, and borrowing limits. A credit score summarises parts of that history into a quick risk signal for lenders.

For example, if two people apply for the same loan, the person with a stronger payment history and lower card balances may receive a better rate. As a result, good credit can save money over time.

Credit scoring is not identical everywhere. Scores vary by country, lender, and scoring model. Even so, several habits usually matter: paying on time, using only a small part of your limit, avoiding too many applications, and checking your report for errors.

This checked infographic explains the main credit habits that usually matter most. The exact weighting can vary by country and scoring model.

Also read: How to Read Financial Statements Even If You’re a Beginner

Why Building Credit Does Not Mean Carrying Debt

A common myth says you must keep a balance on a credit card to build credit. That can be expensive. In most cases, you can use a card for planned spending and then repay the full balance before interest is charged.

For example, you could put $100-$300 of normal monthly spending on a card with a $1,000 limit. If you already planned that spending and repay it in full, you create credit activity without treating the card as extra income.

Therefore, the rule is simple: use credit as a payment tool, not a lifestyle upgrade. If you would not buy something with cash, do not buy it just to improve your score.

Top 10 Smart Ways to Build Credit Safely

Pay every bill on time: Payment history is one of the strongest signals. Set reminders 5-7 days before due dates. In addition, use autopay for the minimum payment as a safety net, then pay the full balance manually when possible.

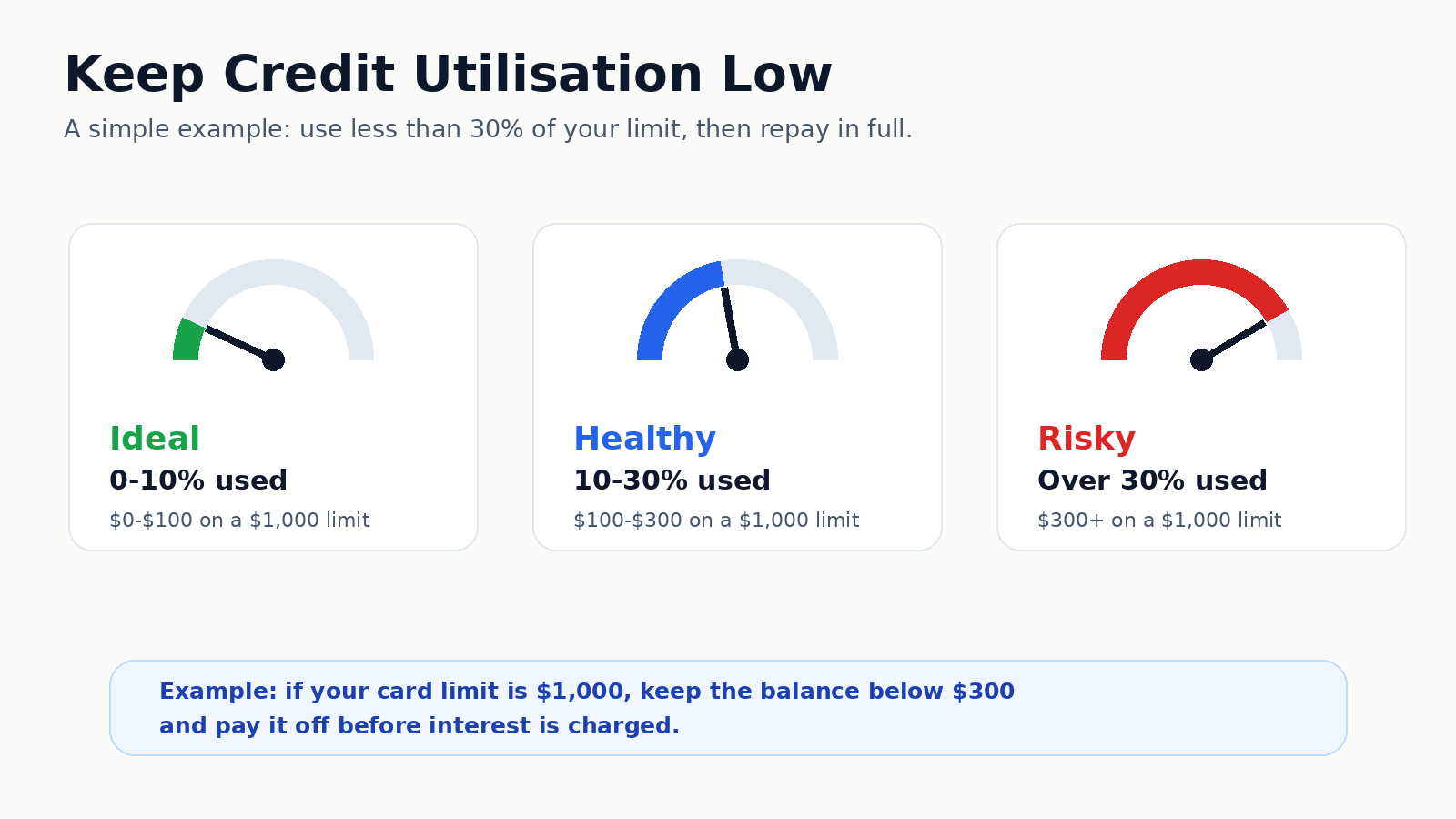

Keep credit utilisation below 30%: Credit utilisation means how much of your available credit you use. If your limit is $1,000, try to stay below $300. For extra safety, aim for 10-20% when your budget allows.

Use credit only for planned spending: Choose one predictable category, such as groceries, fuel, or a phone bill. This keeps your credit use controlled and stops impulse buying from becoming debt.

Pay in full to avoid interest: Many credit cards can charge high interest if you carry a balance. Paying in full gives you the credit-building benefit while avoiding expensive borrowing.

Check your credit report every 30-90 days: A wrong address, old account, or incorrect missed payment can damage your profile. Regular checks help you spot errors early.

Avoid too many hard applications: Several applications in a short time can make you look risky. Space applications by 3-6 months unless you have a strong reason.

Keep old well-managed accounts open: A long positive history can help. If an old account has no annual fee and you manage it well, keeping it open may support your profile.

Consider a secured card or credit-builder product: If you have thin credit, a starter product can help. However, check fees, limits, and repayment rules before signing up.

Report rent or regular payments where available: Some services can report rent or utility payments. This may help if you already pay on time but have little traditional credit history.

Build an emergency buffer first: A $500-$1,000 emergency fund reduces the chance of using credit during a crisis. Saving 10-20% of income for several months can create useful protection.

This checked example shows how credit utilisation works on a $1,000 card limit.

How to Build a Simple Monthly Credit Routine

A monthly routine keeps credit building boring, which is exactly what you want. Spend 20-30 minutes once a month checking accounts, balances, and due dates.

Step 1: choose one card for planned spending only. Step 2: set autopay for at least the minimum. Step 3: repay the full balance after payday. Step 4: check your credit report for errors.

For example, if your monthly card spending is $250 and your income is $2,000, that is 12.5% of income. Keep it planned, repay it quickly, and avoid turning credit into a spending excuse.

A realistic bill-payment setup showing how autopay and calendar reminders can prevent missed payments. The app screens are illustrative, not real product screenshots.

Best Tools and Apps to Monitor Credit by Region

The right tool depends on where you live. However, the purpose is the same: check your report, track changes, spot errors, and avoid surprise applications or fraud.

|

Region |

Tools |

Benefit |

|---|---|---|

|

Global |

Experian, Equifax |

Credit report access and alerts |

|

United States |

Credit Karma, Self |

Score tracking and builder options |

|

United Kingdom / Europe |

ClearScore, MoneySavingExpert Credit Club |

Free score checks and report insights |

|

Advanced users |

YNAB, Monarch Money |

Budgeting that reduces debt pressure |

Before paying for a service, check whether a free report or trial gives you enough value. A $0 tool is better than a $20 monthly subscription you forget to cancel.

Common Credit-Building Mistakes to Avoid

The fastest way to damage credit is to treat it like free money. A higher limit does not mean higher spending power. It only means you have more room to borrow if needed.

Avoid these common mistakes: missing payments, using over 30% of your limit, applying too often, closing every old account, and paying interest just to “build credit”.

Similarly, do not ignore smaller commitments. A phone contract, overdraft, rent-reporting service, or buy-now-pay-later plan can still create problems if you miss payments.

This checked infographic compares safe credit-building habits with common mistakes that can lead to debt stress.

FAQ

Can I build credit without a credit card?

Yes. You may build credit through reported rent, phone contracts, credit-builder loans, or other accounts that report payment history. Availability depends on your country and provider.

Should I carry a balance to improve my credit score?

No. Carrying a balance is not required and can cost interest. Use credit lightly and pay in full whenever possible.

How long does it take to build credit?

Many people need 3-6 months to see early progress, while a stronger history can take 12 months or more. Consistency matters more than speed.

Is 30% credit utilisation always safe?

It is a useful guideline, not a guarantee. Lower utilisation, such as 10-20%, may look better if you can manage it without stress.

Can checking my own credit score hurt it?

Usually no. Checking your own score is normally a soft check. Applying for new credit is more likely to create a hard search.

Final Thoughts

You can build credit without getting into debt by using credit carefully, paying on time, keeping balances low, and checking your report regularly. The best system is simple enough to repeat every month.

Start with one safe habit this week. Set a payment reminder, check your report, or lower your card balance below 30%. Small actions, repeated for 6-12 months, can create a stronger financial profile without debt stress.