A realistic home finance scene showing someone reviewing purchase paperwork, notes and a phone-based budget view. The phone screen is illustrative, not a real app screenshot.

A big purchase can feel exciting until the payment starts squeezing everything else. A new laptop, holiday, sofa, car repair or home appliance may be useful, but poor timing can wreck your budget for months.

Smart spending means planning the purchase before emotion, pressure or discounts take over. In simple terms, you compare the total cost, save in advance, protect your essential bills and choose the safest payment method.

In this guide, you will learn how to plan big purchases without wrecking your budget, using clear numbers, real tools and simple checks you can finish in 20-30 minutes.

What Counts as a Big Purchase?

A big purchase is any expense large enough to affect your normal monthly cash flow. For many people, that might be $500-$1,000. For others, it may be $2,000-$5,000 or more.

The exact amount matters less than the impact. If buying it means skipping savings, relying on credit card debt, delaying bills or feeling stressed for weeks, it deserves a plan.

For example, a $1,200 phone or laptop may be affordable if you save $200 monthly for six months. However, it becomes risky if you put it on a high-interest card with no repayment plan.

Read also: 10 Simple Money Habits That Build Wealth Over Time

Why Big Purchases Break Budgets

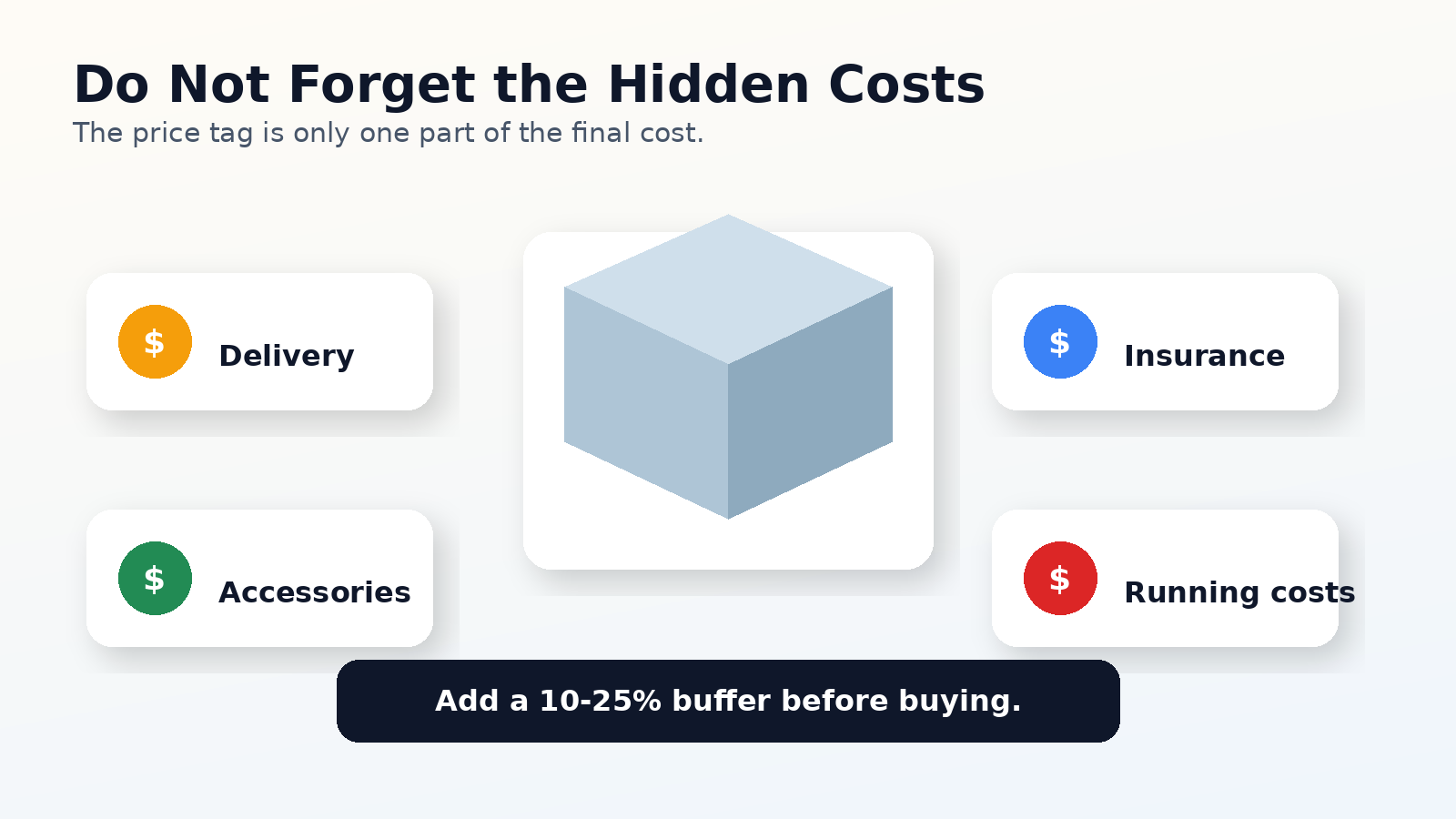

Big purchases often break budgets because people focus on the price tag, not the full cost. Delivery, setup, accessories, insurance, repairs and subscriptions can add another 10-25% to the final amount.

There is also a timing problem. A purchase may look affordable on payday, but it can become painful when rent, food, transport and savings are due later in the month.

A practical rule is simple: if a purchase will reduce your emergency fund below one month of essential expenses, slow down and rebuild the plan first.

This educational image highlights common hidden costs that can make a large purchase more expensive than the sticker price.

1. Define the Real Reason for the Purchase

Before comparing prices, write down why you want the item. Is it solving a real problem, replacing something broken, improving work, saving time or simply giving you short-term excitement?

For example, replacing a failing laptop used for work is different from upgrading a working laptop because the new model looks nicer. The first may protect income. The second may be a want.

Use a two-column note in Google Keep, Apple Notes or Notion: “need” on one side and “want” on the other. This small step can stop emotional spending before it starts.

2. Set a Maximum Price Before Shopping

Set your maximum price before browsing. Otherwise, comparison sites, reviews and limited-time offers can quietly push you from $800 to $1,400.

A good starting point is to choose three numbers: your ideal price, your maximum price and your walk-away price. For a sofa, that might be $700 ideal, $900 maximum and $1,000 walk-away.

This gives you control. If the item passes your walk-away price, you stop shopping instead of negotiating with yourself.

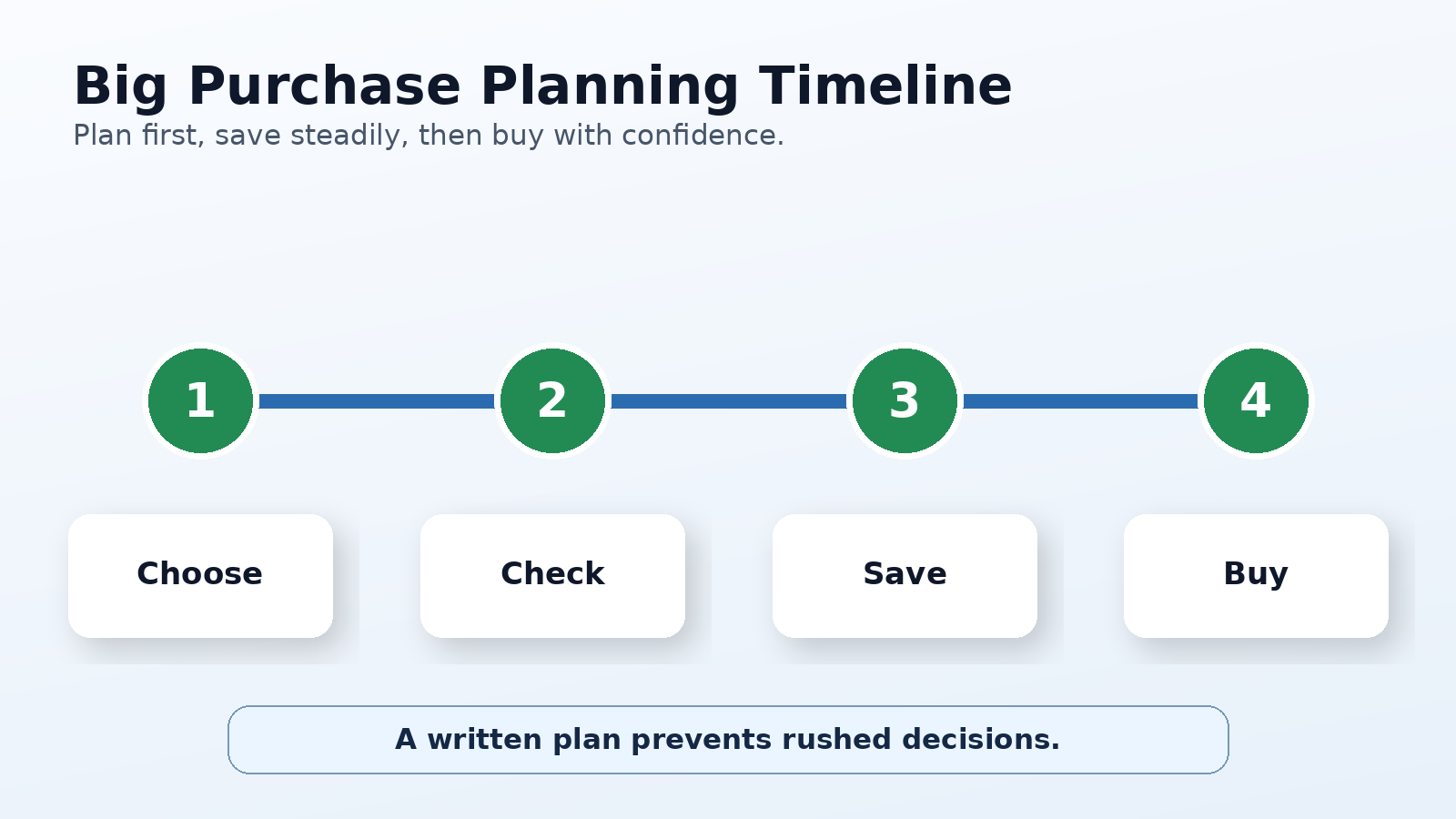

A simple planning timeline shows how to move from idea to purchase without rushing into debt.

3. Check Your Monthly Cash Flow First

Cash flow means the money moving in and out of your life each month. Before a big purchase, check what is left after essential bills, savings and debt payments.

For example, if your monthly take-home pay is $3,000 and your essentials are $2,100, you have $900 before flexible spending. A $300 monthly payment would use 10% of your income and one-third of your free cash flow.

That may be manageable. However, if your free cash flow is only $250, the same payment is too tight.

This checked affordability test shows when a monthly payment may be safe, careful or risky compared with take-home pay.

4. Save First, Then Buy

Saving first is the cleanest way to protect your budget. It also gives you time to compare prices, wait for genuine discounts and avoid panic borrowing.

Try a short saving plan: divide the target price by the number of months before you need the item. A $1,500 appliance in five months needs $300 monthly. A $900 holiday deposit in six months needs $150 monthly.

Use automatic transfers into a separate savings pot. Many banking apps, including Monzo, Starling, Chase and Revolut, let users separate money into spaces, pots or vaults.

5. Use the 24-Hour and 30-Day Rules

For non-urgent purchases, add a waiting period. Use 24 hours for items under $500 and 30 days for items over $1,000.

This delay works because excitement fades. If you still want the item after the waiting period, and the numbers still work, the decision is more likely to be sensible.

For example, save the product page in Todoist or Notion with a review date. When the date arrives, check the price, your budget and whether you still need it.

Read also: How to Compare Subscription Costs Before They Drain Your Budget

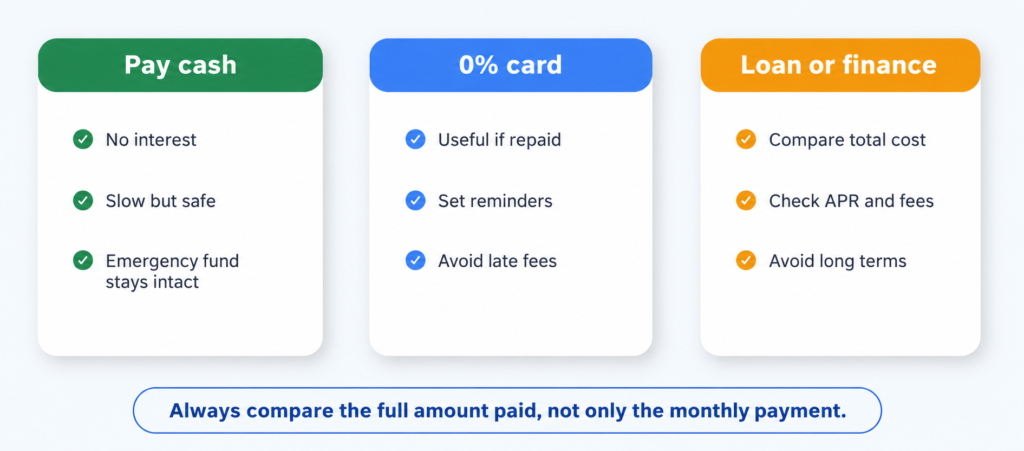

6. Compare Total Cost, Not Monthly Payments

Monthly payments can make expensive items feel cheap. However, the real question is: how much will you pay in total?

A $1,200 purchase over 12 months at 0% interest costs $1,200 if paid on time. But the same purchase with fees or high interest can cost $1,400-$1,700.

Always compare the cash price, interest rate, fees, repayment length and penalties. This is especially important with store finance, personal loans and buy now, pay later plans.

This comparison image shows why the full repayment cost matters more than the monthly payment alone.

7. Protect Your Emergency Fund

A big purchase should not leave you unable to handle a real emergency. If possible, keep at least one month of essential expenses untouched. A stronger target is three to six months.

For example, if your essentials are $2,000 monthly, avoid draining your savings from $2,200 to $200 for a non-urgent item. That leaves almost no protection for repairs, job changes or medical bills.

In contrast, saving gradually lets you buy the item while keeping your safety buffer intact.

8. Use Real Tools to Plan the Purchase

Good tools make the plan easier to follow. Choose one tool for tracking, one for reminders and one place for purchase research.

Global: YNAB helps assign money to priorities; Google Sheets gives flexible tracking; Notion works well for purchase research notes.

United States: Monarch Money gives budget and goal tracking; Rocket Money helps monitor subscriptions and recurring spending.

United Kingdom / Europe: Snoop highlights spending insights; Emma tracks subscriptions and budgets; Monzo or Starling pots can separate purchase savings.

Advanced users: Microsoft Excel or Tiller Money can create custom dashboards for large goals and cash-flow forecasts.

**[ADD MONETISATION OPPORTUNITY HERE]**

9. Plan for the After-Costs

After-costs are the expenses that arrive after the purchase. These often include insurance, maintenance, accessories, delivery, fuel, energy use or subscription fees.

A $900 printer may need ink. A $1,500 laptop may need software, a case and cloud storage. A $4,000 holiday may need luggage, travel insurance, transport and food.

Before buying, add a 10-25% buffer. If the item costs $1,000, plan for $1,100-$1,250 total unless you know the full cost already.

10. Review the Decision After Buying

After the purchase, review how it affected your budget. Did you stay within the plan? Did hidden costs appear? Did the item solve the problem you expected?

This review helps you improve future decisions. For example, if a $1,200 purchase created three tight months, you may decide next time to save for eight months instead of four.

The goal is not guilt. The goal is feedback. Better spending decisions come from reviewing real results, not pretending every purchase went perfectly.

How to Build a Simple Big Purchase Plan

Use this 20-30 minute process before any large expense:

- Write the item and the real reason you need it.

- Set an ideal price, maximum price and walk-away price.

- Add hidden costs, usually 10-25% extra.

- Check your monthly cash flow after bills and savings.

- Choose a saving timeline, such as $100-$300 monthly.

- Compare total cost if using finance.

- Wait 24 hours to 30 days before committing.

For example, if you want a $1,200 laptop and can save $200 monthly, the clean plan is six months. If you need it in three months, save $300 monthly and reduce the specification rather than using expensive debt.

Best Tool Options by Region

Global: YNAB – goal-based budgeting; Google Sheets – flexible free tracking; Notion – research and checklist planning.

United States: Monarch Money – household budgeting and goals; Rocket Money – subscription and spending review.

United Kingdom / Europe: Snoop – spending insights; Emma – budget and subscription tracking; Monzo or Starling – savings pots for purchase goals.

Advanced users: Microsoft Excel – custom purchase calculators; Tiller Money – spreadsheet-powered finance tracking.

FAQ

How much should I save before a big purchase?

Aim to save the full amount when possible. At minimum, avoid reducing your emergency fund below one month of essential expenses.

Is it bad to finance a big purchase?

Not always. Finance can be useful if the rate is low and the payment fits your budget. It becomes risky when you focus only on the monthly cost.

What is the best way to budget for expensive items?

Create a separate savings goal, automate monthly transfers and include hidden costs such as delivery, insurance and accessories.

Should I use a credit card for a large purchase?

A credit card can offer protection or rewards, but only if you can repay the balance in full before interest is charged.

How do I know if I cannot afford a purchase?

If it delays bills, drains your emergency fund, increases high-interest debt or causes stress, the purchase needs a slower plan.

Conclusion: Buy with a Plan, Not Pressure

Planning big purchases is not about never enjoying your money. It is about buying useful things without creating months of stress.

Start with the reason, set a price limit, check your cash flow and save before buying where possible. In addition, compare total costs and protect your emergency fund.

Before your next major purchase, spend 20-30 minutes building a simple plan. That small pause can save you $100-$300, reduce regret and keep your budget steady.